Sponsored By

The African mobile operator predicament with so-called over-the-top (OTT) services has flared up over the past few months as more regulators scramble with the issue of how to deal with the likes of WhatsApp, Skype Ltd. and Viber.

In Morocco, all three mobile operators (Maroc Telecom , Médi Télécom S.A. (Méditel) and Inwi ) moved to block mobile calls using WhatsApp, Skype and Viber, at the apparent behest of regulatory body ANRT. In a statement, the ANRT noted that VoIP services could only be provided by operators holding the requisite licenses to do so.

In South Africa, the country's parliament has held hearings on the regulatory framework governing OTTs, and regulatory body ICASA has indicated it will now look into the matter. Last March, Senegal's regulator ARTP ordered a local operator to reinstate OTT services after the operator had purportedly moved to block them.

Not down with OTT

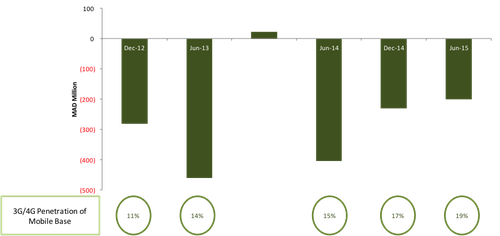

The issue has gained new intensity for a variety of reasons. Operators are feeling a negative financial impact from OTT services, which are hitting three main revenue lines: international voice, SMS (both of which have been declining by 10-30% annually) and, to a lesser extent for now, domestic voice revenues.

To be sure, OTT services are helping drive operator data services revenues too, with data revenues growing in excess of 20-30% a year or more (the fastest-growing revenue line for most).

The problem is the net differential between revenue gains and revenue losses attributed to OTT services. We define this as the net revenue contribution (NRC) of data -- in essence the difference between the incremental gains in data revenue and the losses of voice and SMS revenue over a given period, in absolute terms.

For the most part, we found that many African operators have a negative NRC -- what they are losing on the voice and SMS side is not yet being compensated by what they are gaining on the data side, a potential argument for revenue cannibalization. Even if one does not believe in this cannibalizing effect, there has been enough correlative evidence to spur operators into some form of action.

In addition, operators are now being asked to pay up for 4G spectrum and roll out new infrastructure. Many are concerned they are investing in the tools of their own demise and, in turn, they are putting pressure on regulators to do something about OTT players. Governments are also noticing revenue shortfalls -- lower or flat operator revenue means lower tax revenue, at a time when economic growth is slowing down; the decline in international voice also threatens an important source of foreign exchange, even as African currencies continue to depreciate. Add to that security concerns related to the ability to tap into VoIP calls, and the temptation to block OTT services outright is strong.

Next page: The need for transformation

While the urge to block OTT is strong, what the above trends really highlight is the need for African operators to transform their operating and business models. For one, our research suggests that initially negative data revenue contribution is a feature of the evolution towards data-centric models. While the data net revenue contribution starts in negative territory, it really is a U-shaped curve that turns positive over time as more people use data services, thanks to network effects, accelerated usage and an operating model that becomes more optimized for data services. Once data revenue hits a given level (generally higher than 30% of revenues), its broader contribution should actually be positive. In effect, the negative net contribution phase is a transitionary phase to a data-centric model; how long it stays negative is really more of a commentary on each operator's operating model and innovative approach.

Blocking OTTs could also hurt more than it helps. Even acknowledging the challenge to operators represented by OTT services, such services are now so intricately integrated into usage patterns that they would be extremely difficult to regulate without a materially negative impact on customers that have come to rely on them. Besides contributing to the broader spirit of innovation, the widespread usage of Skype, Viber and WhatsApp have made them critical to small business collaboration and consumer interaction. This is even more critical in Africa where small business (including the informal sector) is critically important for economic development -- and highly price-sensitive. Blocking OTTs is an indiscriminately blunt and shortsighted instrument for a challenge that, in effect, cannot really be legislated away.

African operators have to burn their SMS and voice platform

Ultimately, operator focus in dealing with OTTs should really be at strategic, marketing and operational levels. In fairness to operator management, they often have limited leeway for this at a time they need free rein. One of the most significant challenges facing organizations at different junctures is the need to reinvent themselves to adapt to changing market conditions.

This is where African mobile operators are increasingly finding themselves. But they are victims of their own success at driving profitability so effectively over the years. Investors (and company boards) have become so comfortable with high margins that they look uncharitably at anything that appears to threaten them, notwithstanding how artificial they might have been in the first place. In turn, management is often more rewarded for playing defense than going on offense. Addressing the OTT challenge requires the smart, long view, at the time when operator decision-makers, unfortunately, often appear obsessed with the short view. Many are yearning for market conditions that no longer exist.

In a memo that is now part of corporate lore, Nokia Corp. (NYSE: NOK) then-CEO Stephen Elop once told its staff that they were standing on a "burning platform" and needed to jump off it, transform themselves and move forward. This is where many leading African operators find themselves today. They should forget the deleterious regulatory dilly-dallying on OTT services and jump off that burning platform -- and their boards should let them do it, stock price be damned.

The case for Africa-centric net neutrality

The above would still leave open the broader issue of net neutrality, which the OTT challenge really goes to the heart of. And in this respect, we believe there are legitimate policy reasons for firming up a regulatory framework governing OTTs taking into account African conditions. On a net basis, some African countries will lose tax or forex revenue over time from the rapid adoption of OTT services as popular services are offered by companies with little to no presence in their markets -- if their operators do not transform fast enough, or their own tech ecosystem is not vibrant enough to develop local solutions. At a time when a Netflix Inc. (Nasdaq: NFLX) can launch in 54 African countries without even a single server or employee in most, this is a real policy challenge.

For this reason, we are highly wary of a blanket application of US net neutrality rules to African markets. We believe a deeper introspection of net benefits has to take place, and a framework put in place that, while not blocking OTTs outright (for reasons highlighted above), at least favors companies with local staff and operations more explicitly. The alternative is that governments will look for other ways to address real or apparent revenue shortfalls: regulatory fines, increased taxation, more aggressive tax collection, high spectrum costs, etc. And that, in our view, would be even worse.

— Guy Zibi, Principal Analyst, Xalam Analytics