Sponsored By

Thanks in part to the increased implementation of NFV, service providers are buying into Open Compute Project (OCP) servers at a faster rate, according to a recent market tracker report by IHS Markit.

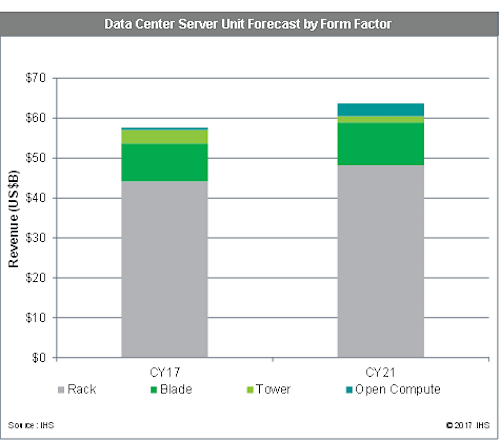

Including tower, rack and blade servers, Open Compute Project server revenue totaled $14 billion in the second quarter of this year, with a growth rate of 41% year-over-year, according to the IHS Markit Data Center Server Equipment market tracker. Overall, OCP servers are projected to represent 7% of the total servers shipped in 2021.

"The ecosystem has been established by the vendors who decided to offer OCP-compliant servers, reducing risk for Tier 2 CSPs to follow. The next wave of OCP adoption will be telcos for network functions virtualization," said Cliff Grossner, PhD, senior research director and advisor for the Cloud and Data Center Research Practice at IHS Markit, in a prepared statement.

The report defined OCP servers as both accepted and inspired designs. While a service provider may use an OCP-based server, in some cases it would modify the server to suit its own needs. For example, at last month's NFV & Carrier SDN event in Denver, AT&T's Tom Anschutz, who is a distinguished member of technical staff, said his company earned Open Compute Project's approval for its XGS-PON optical line terminal. (See Anschutz: Next-Gen NFV Actually Saves Opex.)

During his Denver keynote address, Anschutz noted that open hardware specifications from the likes of OCP can employ more common operational models and that elements -- such as ONIE -- could be used over and over, and from one vendor's box to another manufacturer's box to reduce service providers' opex. (See AT&T's Anschutz: How Open Source Attacks Opex.)

White box servers -- which included all of the vendors that produced rack server hardware with OS software sold separately -- were number 1 in the second quarter in terms of units shipped with a 23% market share.

Overall, total data center server equipment -- which was composed of tower, rack, blade and OCP servers -- totaled $14 billion in the second quarter of this year, which was up 10% from the first quarter and 4% year-over-year.

HPE was the leader in server revenue market share in the most recent quarter with 23%, while Dell was second (19%) and white boxes third (17%). Breaking down 2017 server shipments by categories, cloud service providers were expected to buy 37% of the data servers shipped, telcos 16% and enterprises 48%, according to the market tracker.

Related posts:

— Mike Robuck, Editor, Telco Transformation